China’s dominance of the rare-earths industry is the result of a 40-year campaign by the Chinese state that has given it a market share of between 80% and 90% of the mining, processing and manufacturing of the minerals and their end-use products.

Rare earths are a tiny market worldwide—the total value of mine production is only around US$4 billion—but their uses in high-technology applications have multiplied over the past two decades.

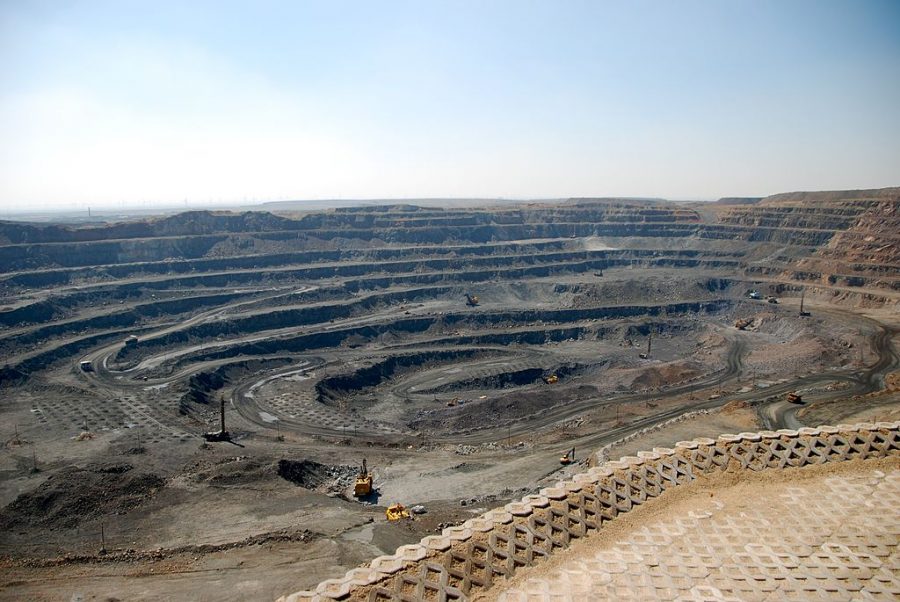

China had been mining rare earths since the 1950s as a by-product from an iron ore mine, Bayan Obo, in Inner Mongolia. It set up a research institute into rare earths near the mine site in the early 1960s, but it remained an essentially cottage industry until the 1970s, when a Chinese chemical scientist, Xu Guangxian—who had played a key role in China’s nuclear program—developed a method of separating the various rare-earth elements, which are usually found combined in the ore.

Production of rare earths from the Bayan Obo mine soared from 1,000 tonnes in the late 1970s to 11,860 tonnes by 1986, which surpassed production in the United States.

The 1970s and the early 1980s were a period of intense resource nationalism around the world. OPEC was formed, and producer groups, with varying aspirations to control market prices, were established in the bauxite, copper, tin, uranium, phosphate and iron ore industries.

As the Cultural Revolution subsided and the administration of Deng Xiaoping began focusing on China’s economic development, exploiting natural resources and adding value to them became a priority. In 1986, Deng approved a national high-tech research and development plan to help China ‘to gain a foothold in the world arena; to strive to achieve breakthroughs in key technical fields that concern the national economic lifeline and national security; and to achieve “leap-frog” development in key high-tech fields in which China enjoys relative advantages or should take strategic positions’.

In 1992, on a visit to inner Mongolia and the rare-earths district of Baotou, Deng famously commented:

The Middle East has its oil, China has rare earth: China’s rare earth deposits account for 80 percent of identified global reserves, you can compare the status of these reserves to that of oil in the Middle East: it is of extremely important strategic significance; we must be sure to handle the rare earth issue properly and make the fullest use of our country’s advantage in rare earth resources.

China’s mercantilist approach to rare earths was reinforced by Deng’s successor Jiang Zemin, who, on a similar visit to Baotou in 1999, declared that China’s task was to ‘improve the development and application of rare earth, and change the resource advantage into economic superiority’.

China’s production of rare earths rose strongly, reaching 50,000 tonnes by 1996 and 120,000 tonnes by 2010.

At least 40% of China’s output was ‘illegal’ production by small-scale entrepreneurs in the south of China who found they could extract rare-earth oxides from clay soils either with strip mining or by soaking trenches with sulphuric acid.

Efforts to shut down these operations, which cause extensive environmental damage, have been only been partially successful, in a striking reminder that the power of the monolithic Chinese state diminishes with the distance from Beijing.

While building its own production, China has also sought to control the output of rivals. In 2005, the China National Offshore Oil Corporation bid US$18.5 billion for the US oil business Unocal. Unocal had large proven oil and gas reserves in Asia which were attractive to the Chinese oil company. Unnoticed during the heated US debates over the bid was that Unocal also owned the only rare-earths mine in the US, Mountain Pass (it was mothballed at the time). CNOOC’s bid raised a political storm in the US which ultimately led it to withdraw.

In May 2009, China Non-Ferrous Mining Company offered Australian rare-earth developer Lynas a financial lifeline after its funding had been torpedoed by the global financial crisis. The Chinese company would buy 52% of Lynas for $252 million and would provide guarantees for a further US$184 million debt package, which would be sourced from China. CNFMC would take four of the eight board seats and be guaranteed a share of its output.

Treasurer Wayne Swan had taken the papers from the Foreign Investment Review Board recommending that the offer be accepted with him to a meeting of the International Monetary Fund in Washington. Swan had earlier signed off on an FIRB recommendation that he approve the purchase by Chinese investors of a 25% stake in another rare-earths prospect, Arafura, which had also lost access to funding following the financial crisis.

In the US, Swan was startled to read a New York Times report detailing China’s dominant stake in the global rare-earths market. He then asked the FIRB to reconsider the Lynas deal. It came back, suggesting a maximum Chinese shareholding of no more than 49.9% and less than half the directors, leading the Chinese to withdraw their bid. Lynas was eventually developed with Japanese government finance.

The most striking example of the Chinese state seeking integrated control of the rare-earths industry was its 1997 purchase of the General Motors subsidiary Magnequench, which had, in the early 1980s, developed and patented the technology for making permanent magnets using the rare earth neodymium (Japan’s Sumitomo Metals patented a different method for making rare-earth magnets at the same time).

In the mid-1990s, GM was going through a period of corporate restructure, shedding ‘non-core’ subsidiaries, and the magnet-making firm was sold to a joint venture of two Chinese state-owned firms for US$70 million. The sale was controversial—regulators demanded a commitment that the Chinese buyers would retain the assets of the business in the United States for at least five years. There were suggestions the sale helped GM gain permission to establish an assembly line in China.

The buyers were impeccably connected: the new Chinese chairman of Magnequench, Hong Zhang, was married to the daughter of Chinese leader Deng Xiaoping, Deng Nan. Under its Chinese ownership, the firm established a parallel permanent magnet-manufacturing business at Tianjin in China. In 2002, the day after the five-year commitment expired, the US manufacturing operations were closed and the entire plant was shifted to China. The US has only regained a fraction of its capacity to manufacture rare-earth magnets.

Chinese investors remain active in securing stakes in rare-earth prospects around the world, including in listed Australian rare-earths companies Arafura and Northern Minerals.

Fears that China may use its dominant position as a weapon in its trade war with the US were sparked when China’s president Xi Jinping visited the leading rare-earths miner and magnet manufacturer JL Mag in June this year, a few days after the US had announced it would ban the export of technology-sensitive products to Chinese telecommunications giant Huawei.

He said rare earths were an important strategic and non-renewable resource, but he emphasised the importance of adding value through their application. ‘We should firmly grasp the strategic basis of technological innovation, master more key core technologies and seize the commanding heights of industry development’, he said.