The Turnbull government’s new Defence White Paper promises to increase defence spending to 2% of GDP by 2020–21—three years earlier than Tony Abbott promised. Better still, they’ve provided an explicit table of Defence funding across the forthcoming decade (see DWP p.180). Not since the early 2000s has a government been this willing to open up its books and be held to account. It was a commendable step.

Looking closely at the numbers, an interesting picture emerges; it appears as though the early attainment of 2% of GDP is an artefact of declining nominal GDP expectations. That’s not to take anything away from the government—they unambiguously made good on their promise—but if the numbers are out there, they deserve to be analysed and understood.

In the table below, the nominal (including inflation) funding figures from the DWP are given, along with the annual year-on-year nominal growth rate. In the lower part of the table, the funding is presented in real 2015–16 dollars assuming 2.5% inflation.

Two things surprised me about the figures. First, the growth rates were somewhat below what I’d anticipated. Second, the early attainment of 2% of GDP seemed an unlikely concession from the taxpayer’s guardians in Treasury and Finance. So I looked up the explicit GDP figures from the 2015–16 mid-year update to see what’s going on. It turns out that projected nominal GDP growth is now significantly slower than previously assumed, which explains both the slower growth in defence spending and the earlier attainment of the percent GDP target.

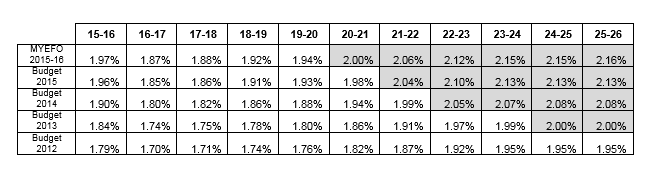

The easiest way to see this is to take the nominal defence spending figures from the DWP and calculate the share of GDP as in successive Treasury projections. This is done in the table below. Because treasury only gives numbers four years out (i.e. out to 2018–19 in the latest update), the latter years have to be estimated by assuming some rate of nominal GDP growth. The key is to realise that the rate of GDP growth assumed by the government was small enough for defence funding to reach 2% of GDP in 2020–21. A little arithmetic shows that nominal GDP growth has to be less than 5.2% for defence spending to reach 2% of GDP in 2020–21. In comparison, the 2013 National Commission of Audit assumed nominal GDP growth of around 5.7% around that time (which is the figure I’ve previously used for modelling purposes). Half a percent can make a big difference once the magic of compounding kicks in.

The deterioration in nominal GDP growth has, in effect, made the attainment of spending 2% of GDP easier and brought it forward by three years. One way to see this is to look at successive Treasury projections of GDP and calculate the share of GDP that today’s DWP funding would represent. This is also done in the table below. In each case, the growth in GDP after the last available year in the Treasury papers has been projected out using the (manifestly modest) 5.2% discussed above. In the earlier budgets, the rate of GDP growth in the latter years would have been higher, meaning that the GDP share of defence spending would have been lower still.

Three points are noteworthy:

First, changing expectations of GDP growth can have a significant impact on the measured GDP share of defence spending.

Second, recalling that the original promise was to reach 2% of GDP in 2023–24, it looks as though funding in the DWP was conceived on the basis of the 2014 Budget’s projections of GDP growth. That conjecture is consistent with the timing of the WP process. (The overshoot can probably be accounted for by the deterioration in the Australian dollar).

Third, the accelerated attainment of the magic 2% figure reflects falling nominal GDP rather than a more ambitious approach to equipping and expanding the ADF.

If nothing else, the foregoing analysis highlights the shortcomings of GDP share as a planning basis. Fortunately, the DWP dispenses with the 2% target and instead fixes defence funding in dollar terms for the next decade (and with adjustments for foreign exchange risk). This severing of the link with GDP is sensible and pragmatic. Nonetheless, I fear that the 2% target will continue to haunt the discussion of defence funding for years to come.