What a difference a year can make. Twelve months ago, it looked like the government had all but abandoned the ambitious plans set out for the ADF in the 2009 Defence White Paper. More than $20 billion of promised defence funding had been cut or deferred over the preceding three years. Last year, funding fell in real terms by more than 10% pushing the defence share of GDP to 1.6%—the lowest level since 1938.

What a difference a year can make. Twelve months ago, it looked like the government had all but abandoned the ambitious plans set out for the ADF in the 2009 Defence White Paper. More than $20 billion of promised defence funding had been cut or deferred over the preceding three years. Last year, funding fell in real terms by more than 10% pushing the defence share of GDP to 1.6%—the lowest level since 1938.

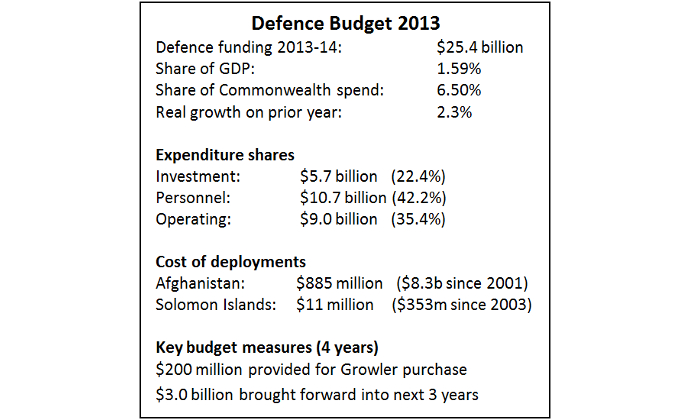

This year things look very different. Defence spending is again on the rise, and the government has released a new Defence White Paper essentially recommitting itself to the capability goals of 2009 and then some. On current plans, the defence budget will increase in real terms by 2.3% next year to reach $25.4 billion, and then continue to grow for another three years to $28.6 billion (all measured in today’s dollars) to deliver an average of 3.6% real growth over four years.

But that’s only the start. If the government makes good on the $220 billion of financial guidance for the six years that follow, there’s enough money available to grow the defence budget to $33.2 billion by 2022 at an annual real rate of growth of 2.5% per annum.

But don’t pop the champagne corks just yet. The seemingly impressive growth is coming from a low base. In the 48 months between the release of the 2009 and 2013 Defence White Papers, around $20 billion of promised funding was lost in the headlong rush to get the Commonwealth’s books out of the red. As things stand, it will be two more years before defence spending rises out of the hole that was dug in search of a surplus.

Is there enough money?

Is there enough money?

Because of the secrecy surrounding the actual funding promised back in 2009, it’s hard to say precisely how much less money there is today compared with back then. But taking the 2009 funding commitment at face value, the shortfall is in the vicinity of $30 billion for the period 2009 to 2022. Consistent with this, the share of GDP will remain below 1.7% for the next decade.

Of course, GDP share is a poor measure of the adequacy of defence spending; it’s been trending down since the end of our involvement in Vietnam as the economy grew. What really matters is whether the government has committed enough money to deliver the defence force it says we need. The short answer is that it has not.

Here’s how things stand. The planned scale and sophistication of the ADF has not been reduced appreciably since the 2009 White Paper. In fact, it’s grown in some key areas. Not only did the new White Paper announce the purchase of 12 previously-unplanned Growler configured Super Hornet aircraft, but we’re now planning to keep the Super Hornets in service concurrent with the yet-to-be-acquired F-35 Joint Strike Fighter out to at least 2030. As a result, the prudent strategy of consolidating the RAAF’s fast jet fleets has been abandoned at the cost of much higher personnel and operating expenses in the years ahead. Similarly, the government’s decision to suspend consideration the off-the-shelf options for the Collins submarine replacement only leaves the two most expensive and risky options on the table.

So even if the 2009 Defence White Paper was affordable—and it probably wasn’t in the long term—it follows that with more capability and less money the 2013 Defence White paper is not.

The same conclusion can be reached by looking at the cost of maintaining a state-of-the-art military force. US data going back to the 1950s shows that the unit cost of acquiring and operating ships, planes and troops has grown on average at around 3% per annum above inflation. With only 2.5% growth on the horizon, we’ll be lucky to maintain the force we have, let alone expand it.

To the extent that there’s been a political debate over defence spending, it’s been cautious and low key. Both sides ‘aspire’ to grow defence spending to 2% of GDP when circumstances allow, without explaining the merits of that symbolic figure. More critically; neither side of politics is willing to say where they would cut the ADF to close the gap between means and ends, nor are they willing to head off such cuts by making a firm commitment on defence spending. So we have bipartisan make-believe.

Future prospects

Things could get worse. This year’s boost to defence spending was a direct consequence of the government’s failure to achieve a surplus. Had a surplus been within reach, the defence budget would have undoubtedly come under renewed pressure. It’s clear that the $21 billion fiscal blow out created room for the additional defence funding granted this year. There’s a binary calculus at play. Because the Australian Government’s net debt is small in absolute terms, the further accumulation of debt is of political concern only if it prevents a surplus. With a surplus beyond reach for the moment, the impediments to spending were weakened. The Treasurer’s loss became the Defence Minister’s gain.

But we’re not in surplus yet. Whoever comes to government in September will want to get out of deficit before they face the electorate again. And at some point we’ll be back where we were last year, with defence spending being squeezed to help get the budget over the line—just as occurred following the recessions of the 1980s and 1990s.

One of the reasons that both sides of politics are reticent to commit to a long-term figure for defence spending is the substantial uncertainty over future tax revenues. Economists all around town are busying themselves trying to understand the extent of our ‘structural deficit’, a malady we picked up in 2007 but nobody bothered telling us about until now.

This much appears clear: the surplus promised for this year became a deficit due to several factors, the most important of which was the deterioration in our terms of trade. That is, the rate at which our exports generate revenue in our own currency. Between its peak in late 2011 and the end of 2012, Australia’s terms of trade fell by 17%.

The government’s current fiscal projections are based on our terms of trade only declining by a further 2.5% between now and 2015. If it falls further, revenues will decline and the government’s fiscal situation will worsen. We are not out of the woods yet. If events over the past few years have taught us anything, it’s that defence spending is at the mercy of the uncertain health of the government’s finances.

What’s going on?

Notwithstanding the fiscal breathing space created by the failure to achieve a surplus, this year’s boost to Defence was not pain free for the government. While Defence got more money in this budget, other areas were being cut. Consider this: the full cost of the Growler acquisition ($3 billion) is higher than the savings from scrapping the Baby Bonus ($2.5 billion), and there’s no question about the relative political worth of the two items. Defence rated one mention in one sentence in the Treasurer’s budget speech. For better or worse, there are no votes in defence at this time.

Why then has the government renewed its commitment to defence at some political cost, yet presented a manifestly underfunded plan? The most positive interpretation is that they are hedging against adverse strategic developments; on the one hand retaining the ambitious plans of 2009, while on the other providing only enough money to keep things ticking over.

The new White Paper provides surprisingly few hints at what’s behind the government’s thinking. Carefully drafted to avoid giving alarm to anyone, it almost begs the question of why we need to spend so much on cutting-edge military equipment. China was left unperturbed and we were left scratching our heads.

As always, actions speak louder than words. Let the academics squabble over whether the Indo-Pacific is in fact a ‘system’ as learnedly asserted in the White Paper; if you want to know what’s going on, follow the money.

Two developments are noteworthy. In the maritime domain the additional cost and risk of a bespoke submarine project has all but been accepted. Rather than live with the limitations of a short-range off-the-shelf submarine, we are going to pursue boats capable of operating far into North Asia. In the air domain, we are going to have a mixed fleet of the best combat aircraft we can buy, aircraft of sophistication beyond anything likely to emerge in Southeast Asia (apart from our close friend Singapore).

On both counts, the implication is the same. The government is hedging against a serious disruption in the broader strategic environment—a disruption of the sort only conceivable if the US–China relationship confounds the White Paper’s optimistic outlook.

Reality bites

The description of the present situation as a hedging strategy is probably more charitable than accurate. In reality, it looks more like a case of doublethink. We want a strong defence force, but we don’t want to pay for a strong defence force. So full steam ahead, we’ll plan for what we want and hang the consequences.

Of course there’s nothing new in any of this. The same thing happened in the 1987 White Paper and again in 2000. In each case, reality soon asserted itself over wishful thinking. The reckoning for the 1987 White Paper was the 1991 Force Structure Review, which cut personnel numbers to free up money for investment in high-end equipment. In 2003 the opposite happened when the Defence Capability Review cut existing air and maritime platforms but preserved plans to expand the land force.

The outcomes in 1991 (at the end of the Cold War) and 2003 (at the start of the War of Terror) were products of their time. What they had in common was that they adjusted the force structure to meet the demands of the present and the perceived challenges of the future. Each tried to manage strategic risk in light of limited resources.

So what will the reckoning for the 2013 White Paper look like? One thing is sure; it will have to face up to the perennial question of Australian defence planning: the balance between the Army and the capacity to transport it, and high-tech air and maritime platforms. With the Army returning home to barracks, the natural tendency will be to repeat 1991 and shift resources to investment for the Navy and Air Force. But our experience in East Timor and Solomon Islands should temper that impulse.

Another serve of Magic Pudding

The other thing that will certainly emerge in the years ahead is a renewed push for efficiency within Defence. Although worthwhile reform continues on several fronts, the savings targets of the Strategic Reform Program have been set aside. Given that the scale of claimed savings was surely exaggerated, this is no great loss.

On the surface, the prospects for further real savings look promising. It’s clear that the organisation grew top heavy and bloated in the good times of the 2000s when executive and middle management positions exploded in the civilian and military workforces. But it’s unlikely that savings on a sufficient scale to make current plans affordable will be found by trimming the upper ranks, and equally so for the decision to reduce civilian numbers by 1,000 over the next 4 years.

The prospects for savings from another round of outsourcing aren’t great either. Apart from having only a limited number of functions left to be privatised, replacing public servants and military personnel by contractors at best yields a savings equal to the difference between two large numbers. And the durability of such savings depends on the relative business acumen of Defence and its commercial counterparties. Nothing is assured.

So, by all means, let’s produce as lean and efficient an organisation as possible—but don’t pretend that it will be enough to balance the books. Greater efficiency will not remove the need to make hard decisions.

Getting on with the job

In the meantime, Defence needs to get on with the job of delivering. In a sense, this budget has given them a second chance. Performance over the next few years will be critical to the confidence that the government and public has in Defence. Two areas are likely to present particular challenges: personnel and procurement.

As things stand, the uniformed strength of the ADF is fully 1,900 positions below what was budgeted for. A number of factors are probably behind the shortfall. Some people have probably been attracted away to better paying jobs. It’s no surprise that highly trained military tradespeople are valued by civil employers. At the same time, the drawdown from operations will make military service less attractive to many people. Whatever the reason, it will be hard to argue that the ADF should have a strength of 59,000 if Defence can’t recruit and retain that number of people.

On the procurement side, there has been some encouraging progress. The rate of project approvals has increased compared to past years (though it still remains well below planned levels), and DMO reports improvements in delivering projects on time and within budget. This is all good. The problem ahead is that the rapid increase in acquisition spending planned over the next few years greatly exceeds anything that’s been achieved over the past fifteen years. Just as with personnel, if DMO starts to hand money back unspent the temptation will be to give it less money to spend.

In the longer term, the biggest procurement challenge will be the raft of domestic maritime projects reconfirmed in the new White Paper. On the positive side, the government is moving things along in several areas, including by spending real money to make a start on what will be the most expensive defence project in Australian history, the Future Submarine. Less encouraging is Defence’s shipbuilding plan released alongside the White Paper. Developed in consultation with local industry, the new plan touts potential savings in the ‘tens of billions of dollars’. Yet on close examination, its concrete proposals appear more likely to add to the cost that the taxpayer will have to shoulder out to mid-century.

With shipyards lobbying on the front page of newspapers, and unions threatening to strike if orders for more vessels aren’t forthcoming, we urgently need a rational approach to shipbuilding that puts efficiency above vested interests.

Conclusion

After four years of cuts, defence spending is on the rise again. But the growth is occurring from a low base, and in absolute terms funding remains well below what was promised back in 2009. Yet plans for the ADF remain as ambitious as ever.

There’s a Groundhog Day feel about this year’s budget and the broader plans for the ADF now on the table. As always seems to be the case, there is a gap between means and ends that needs to be closed. While this might be explained as a hedging strategy, we risk wasting money in areas that will eventually have to be cut if additional funding is not forthcoming.

In the meantime, it’s up to Defence to get on with the job. Challenges in the areas of personnel and procurement are certain to arise in the years ahead, and the government’s willingness to deliver more money will be tempered by how well Defence delivers on both counts.

Mark Thomson is senior analyst for defence economics at ASPI. Image drawn by John Shakespeare. Reproduced courtesy of the artist and the Sydney Morning Herald newspaper.

Note: The table has been amended to correct a typographical error. The cost of deployment to Afghanistan mistakenly read ‘billion’.